Inflation at the Border: How Road Accessibility Dictates Consumer Prices

In April 2026, Armenia recorded 5.35% inflation, which was the highest rate since mid-2023. In May, this rate had already decreased to 4.24%. A study of statistical data shows that this price shock is almost entirely manifested in the food market and is periodic in nature, intensifying in winter and easing in the summer months. The sharpest inflation recorded in 2026 is mainly due to the disruption of traffic on the logistics highway that ensures price stability.

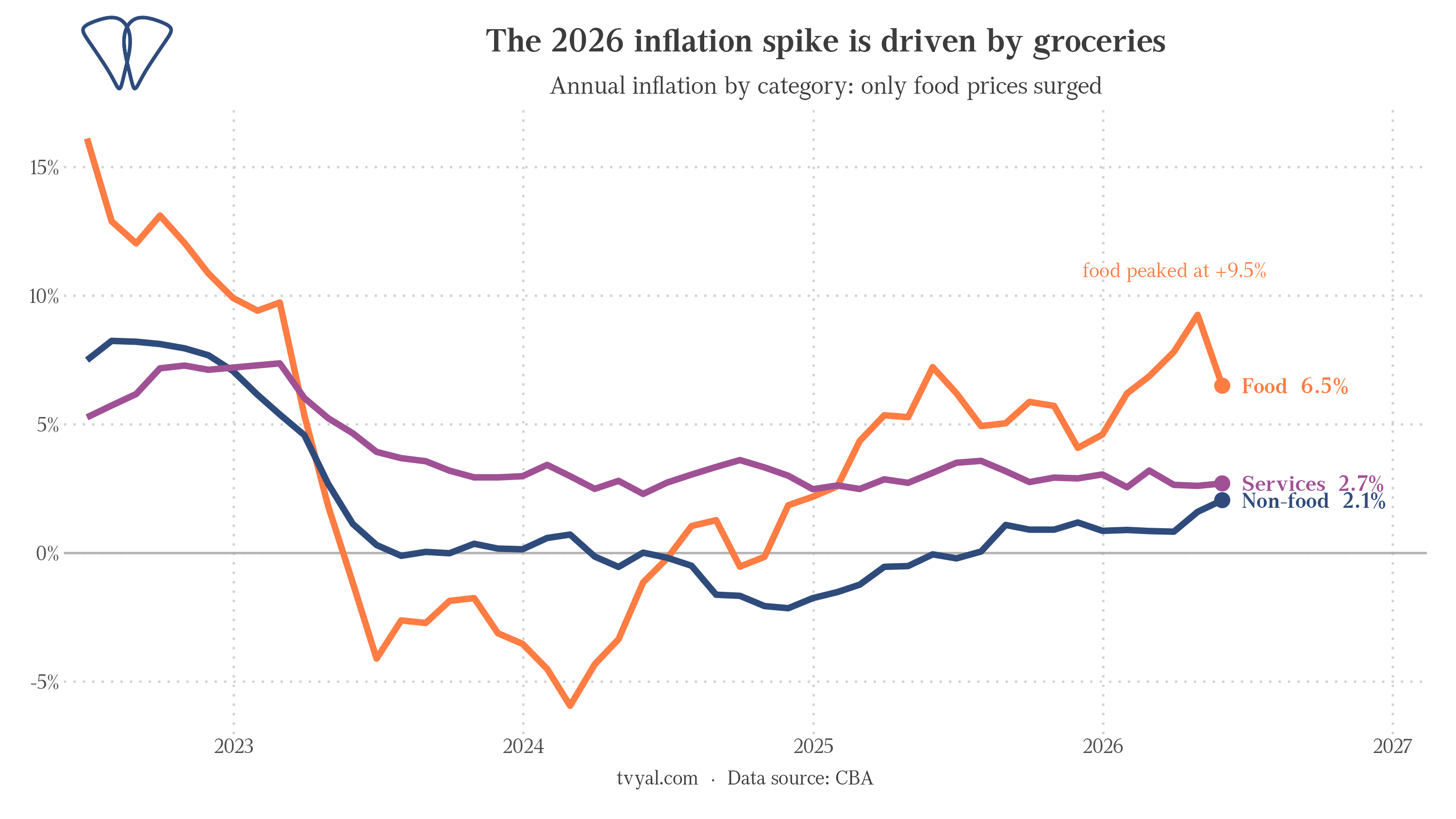

Inflation is driven by the food market, not the domestic economy

Food prices rose by 9.5% year-on-year in April, before falling to 6.5% in May as the first batches of agricultural products entered the market. Food products make up about a third of the consumer basket of Armenian households, so food price fluctuations directly affect the Consumer Price Index (CPI).

The remaining components of the consumer basket did not show significant changes during the year. Inflation in the services sector is around 2.7% (compared to the maximum indicator of 7.2% recorded at the end of 2022), and in the non-food goods market, inflation is 2.1%. In essence, the current inflation does not exhibit the “sticky” nature of demand, which was characteristic of the economic situation at the end of 2022 and was more difficult to manage. This inflation is a consequence of the food supply shock, which is directly due to the logistical problems recorded on the Armenian-Iranian border.

The separation of the mentioned factors is key from the point of view of choosing the appropriate monetary policy instrument. In the case of combined inflation of wages, rents and services, the Central Bank usually uses the tool of increasing interest rates. The food supply shock has a different logic: the situation self-regulates in parallel with the restoration of the normal course of cargo transportation, which suggests that the optimal behavior of the Central Bank in this case is to leave the refinancing rate unchanged and wait.

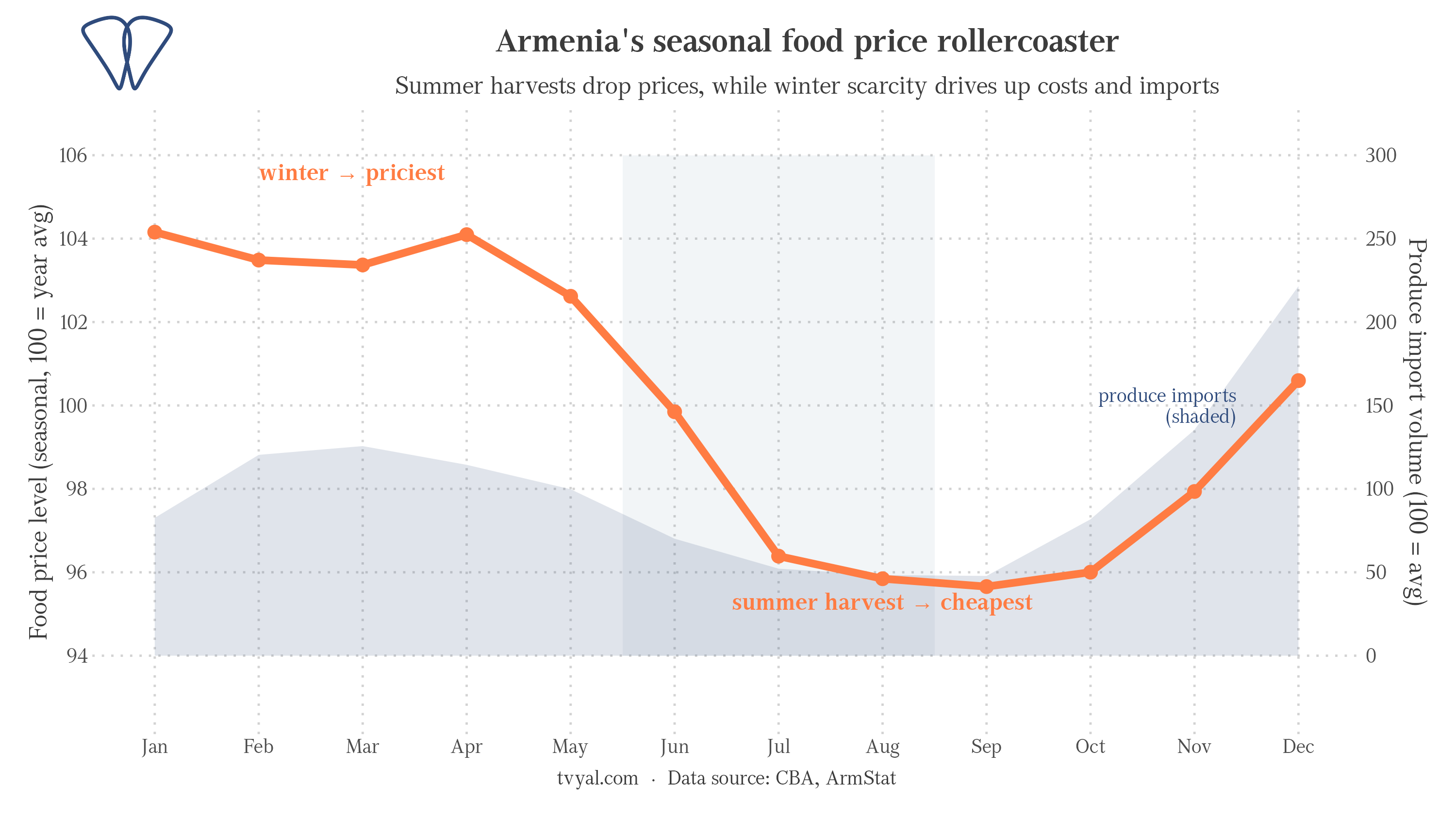

Strong seasonality in food prices

In Armenia, food product pricing has a very regular seasonality. The maximum price level is recorded in the winter months, in parallel with the consumption of local agricultural products, and the minimum level is observed at the end of summer, as a result of a sharp increase in the supply of local crops on the market. During the same period of falling local supply and rising prices, there is an objective need to expand import volumes in order to meet domestic demand, but in the winter months, both the Lars and Meghri borders have a difficult crossing problem. This sharp problem does not affect the price of grain and energy sources, which are brought in advance and stored, but it significantly affects the prices of fruit and vegetables, which are the main non-monetary inflationary stimulus.

Such fluctuations are not typical for the vast majority of developed economies. In the case of the Republic of Armenia, this phenomenon is highly pronounced, which indicates a systemic specificity and vulnerability.

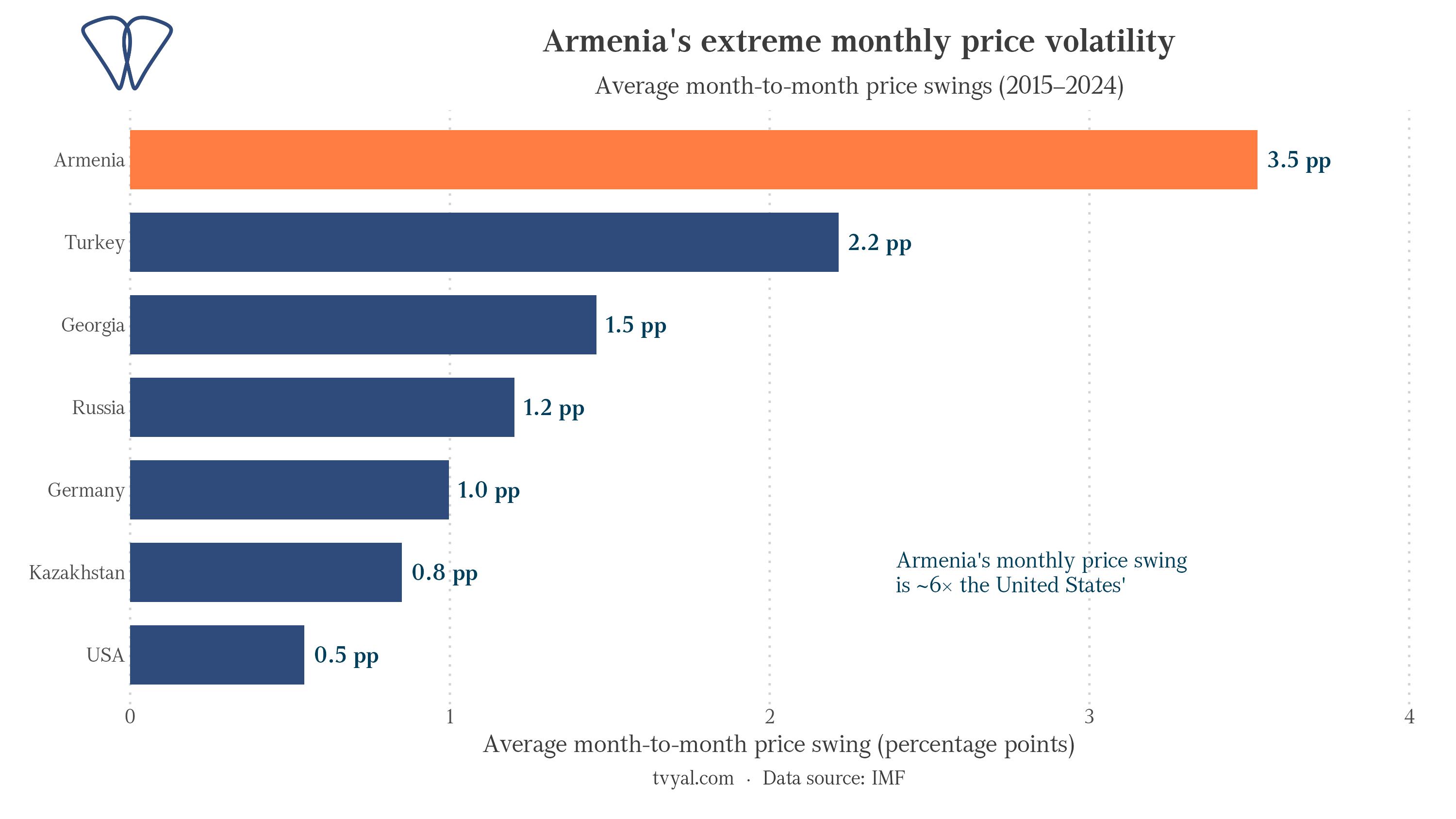

Among all the countries in the world, only economies at war or in a phase of hyperinflation (such as Sudan, Venezuela, Syria and Lebanon) record greater monthly price volatility than Armenia [1]. For comparison, even Turkey, which has a high-inflation problem of its own, has milder monthly fluctuations than Armenia, which is otherwise relatively stable macroeconomically. Moreover, many stable economies whose food share in the consumer basket is just as high show far milder swings. Therefore, the problem is not due to consumption volumes, but to the physical accessibility of the supply routes.

One mountain pass supply route

The logistical nature of the inflation problem is often overlooked by analysts. During the winter months, a significant portion of fresh agricultural produce is imported into Armenia from the Islamic Republic of Iran, through the only customs point in Meghri and a mountain highway at an altitude of 2,535 meters. Iran is the largest supplier of fresh winter agricultural produce to Armenia. The maximum volume of supplies is recorded in December, after which, in January, imports are reduced by about 66% [2]. The decrease is recorded precisely at the time when local reserves are at their lowest, which is due to the objective difficulties of passing the mountain pass in severe weather conditions.

Unlike fuel or grain, which can be stored for a long time, perishable goods require uninterrupted and prompt transportation. Due to this circumstance, any road closure leads to a sharp increase in prices within just weeks.

In the case of Armenia, the pronounced seasonality of inflation is essentially a logistical problem, which is manifested through monetary indicators.

In 2026, the problem was not only due to heavy rainfall. The southern land route was disrupted by the war in March, the most important period when import demand was most pronounced. This directly caused the April inflation rate to peak at 5.35%.

Forecasts and expectations

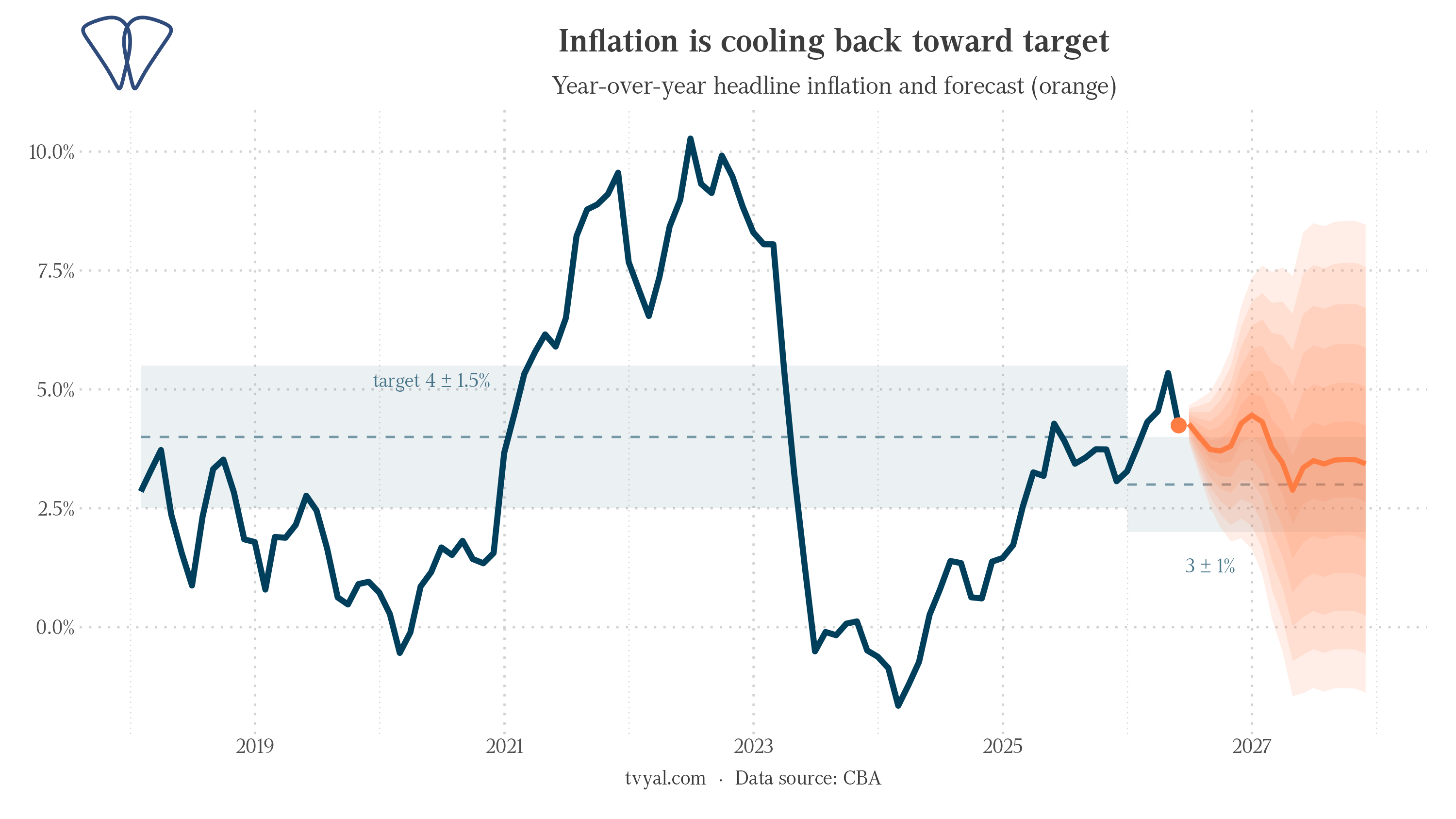

So far, the Central Bank of Armenia has refrained from using monetary policy instruments. At all meetings this year, the refinancing rate has been maintained at 6.50%, slightly above the neutral level of 6.25%. The logic of the Central Bank is based on the assumption that monetary policy is aimed at managing medium-term inflation expectations, rather than neutralizing short-term or seasonal shocks. After all, changing the interest rate cannot restore the passability of the mountain pass [3]. Macroeconomic forecasts are consistent with this approach: as a result of the summer harvest and the fading of the base effect, overall inflation is expected to return to the target range.

It should also be noted that the inflation target has also been revised this year. In January, the Central Bank reduced the target from 4% to 3%, while narrowing the permissible range of fluctuations to +/- 1 percentage point. Therefore, the April figure was within the old upper target threshold, but significantly exceeded the newly set target.

However, there is one statistical indicator that indicates hidden systemic risks. Core inflation, which excludes highly volatile food and energy prices, has risen steadily in all months of the year, reaching 5.0% in May and even exceeding the headline inflation rate. When core inflation exceeds the headline inflation rate, this indicates that the impact of the food shock is likely to be transmitted to wages and other sectors of the economy. Thus, short-term seasonal inflation turns into a large-scale macroeconomic problem, requiring direct intervention by the Central Bank.

Therefore, the main macroeconomic indicator to watch should be not headline, but core inflation. Headline inflation will decrease in accordance with seasonality. If a decrease in core inflation is recorded in parallel, this will prove that the CB’s wait-and-see policy was justified, and the 2026 indicators were due solely to the failure of the mountain pass. However, if core inflation continues to rise while headline inflation falls, this will indicate the continuation of this shock, which will inevitably lead to a revision of the refinancing rate and a tightening of monetary conditions.

Links

[1] Consumer Price Index, Monthly, by Country // International Monetary Fund — imf.org

[2] Foreign trade by product type, fresh agricultural products (HS 07–08) by country of origin and month // Statistical Committee of the Republic of Armenia (Armstat) and UN Comtrade — armstat.am, comtradeplus.un.org

[3] Monetary Policy Program 2026 Q1 and Refinancing Rate Decisions // Central Bank of the Republic of Armenia — cba.am