A Harvest With Nowhere to Go: How Armenia's Economy Got Stuck at the Russian Border

This year the apricot harvest came in late, which at first looked like good fortune. Then, on June 11, Russia closed its border to apricots, along with cherries, plums, peaches and grapes. These were the latest additions to a list of bans that had been growing since the end of May. For these crops Russia is not one market among several; it is effectively the only one. More than 90 percent of Armenian apricots, cherries, tomatoes and cut flowers are sold to that country and almost nowhere else. With the borders to Turkey and Azerbaijan closed, there is no alternative route north for the goods that used to travel there. A crate of perishable apricots cannot wait for a new buyer to appear. The loss of that market translates directly into financial losses, and those losses can leave farming households without the means to plant again next year.

The official explanation is phytosanitary: pests and quality. The timing points to something else. The bans followed Civil Contract’s election victory and Yerevan’s louder talk of EU integration, and they read more like economic pressure than inspection [1]. The Central Bank of Armenia estimates that, if the restrictions hold, the economic damage could reach 2% of GDP [2]. That figure is realistic, and we return to it below, but it captures only part of the risk, not the whole of it.

A ban matched to the harvest

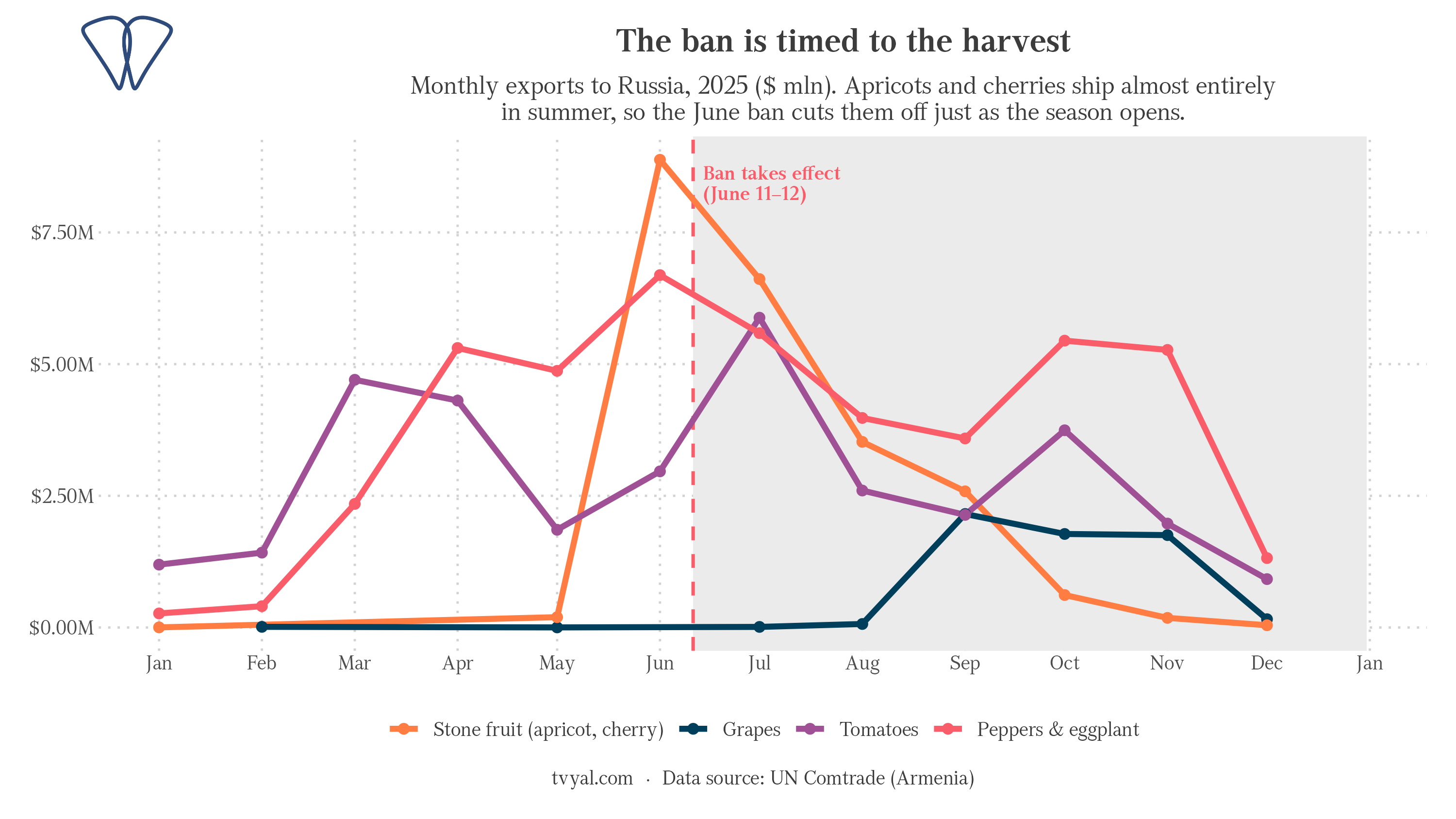

The restrictions came in stages. Cut flowers were banned first, on May 22. Then came the brandy and wine of three named producers, then Jermuk mineral water, then tomatoes, cucumbers, peppers and strawberries. Fish, apples, eggplant and dried fruit followed. On June 11 the sweeping order arrived: a block on the entry of every good subject to quarantine control, and on its transit through Russia to the other countries of the Eurasian Economic Union [1]. Over six weeks, one product group at a time, almost the entire basket of fresh Armenian produce was shut out.

The seasonality of these exports tells the story. Apricots and cherries are summer crops: in the first four months of 2026 their exports to Russia were essentially zero, because the season had not yet begun. The June 11 ban lands exactly as that season opens, wiping out this year’s expected income from stone fruit before any of it is earned. The schedule was clearly drawn up with the harvest calendar in mind. State subsidies cannot fully offset this. Tomatoes and cut flowers keep for only a few days, while reaching the European market takes about two weeks and the right certificates.

Russia, the only market that counts

For years economic policy rested on the idea of “diversification”: reduce dependence on Russia and open up the European, Middle Eastern and Chinese markets. The aim was right, but since 2018 the opposite has happened. Armenia’s trade dependence on Russia and the EAEU has not eased; it has deepened.

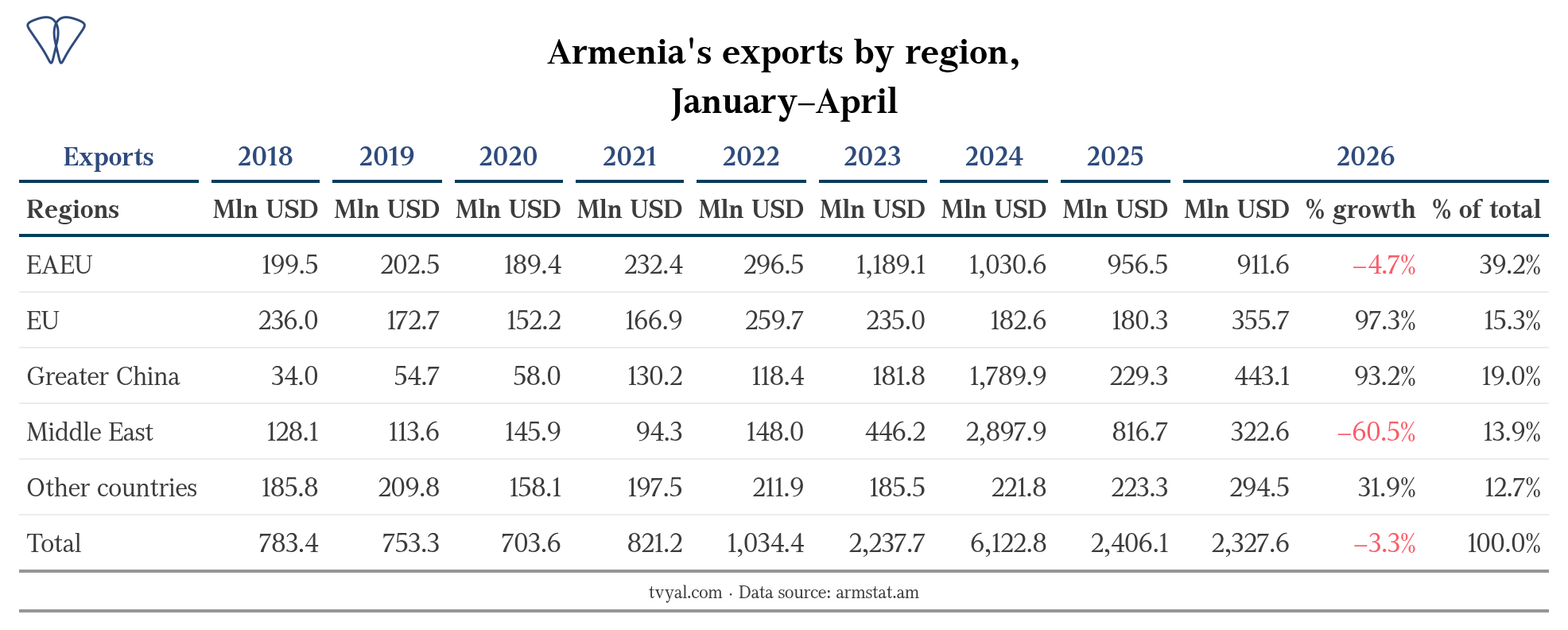

In the first four months of this year the EAEU took 39% of total exports, the European Union 15%. At the start of 2018 the picture was the reverse: the EU was the main market at 30%, the EAEU 26%. Today’s position is far more exposed, because the ties to the Russian market have grown tighter, not looser. Instead of diversifying and spreading the risk, we concentrated it.

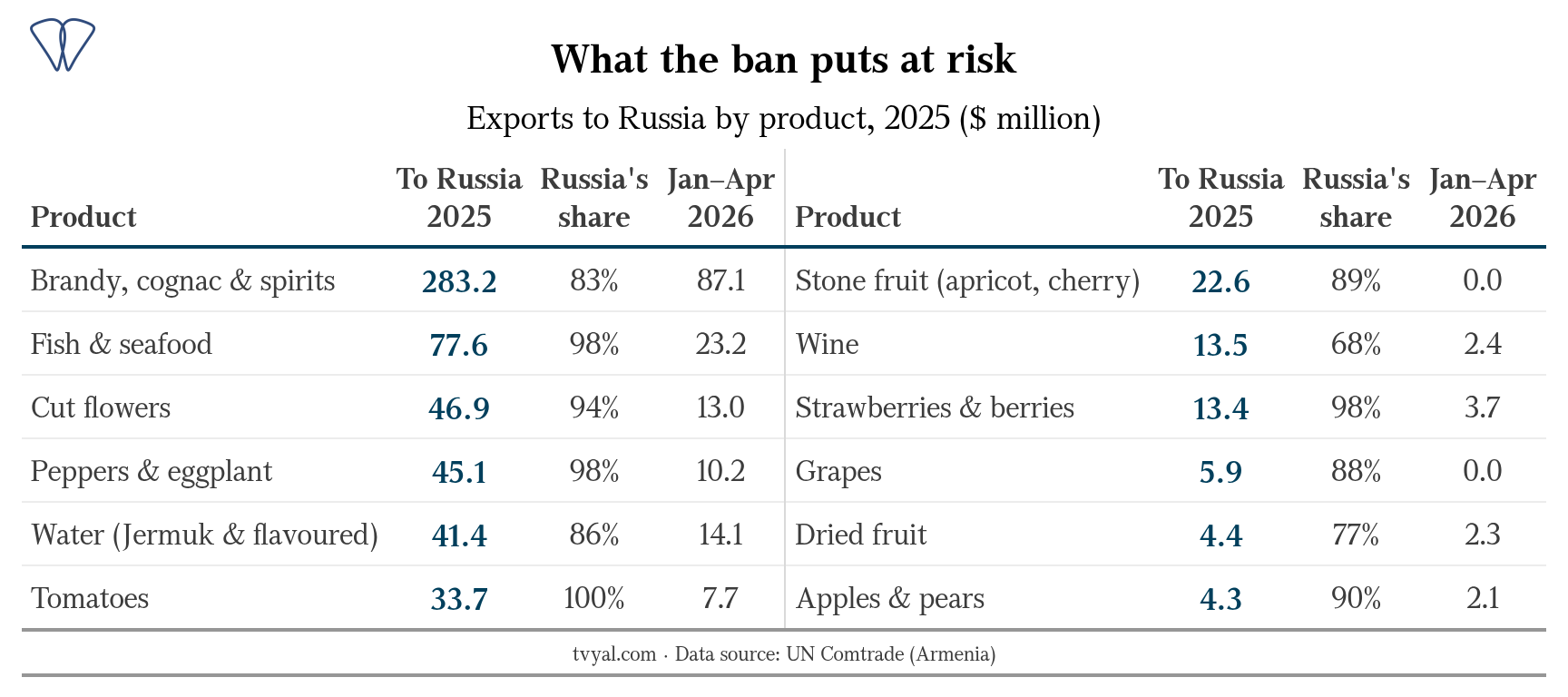

Lining up the banned goods shows where the weight really sits. Brandy alone accounts for about $283 million of exports to Russia, roughly half of everything on the list. Because brandy and Jermuk water do not spoil, their losses can be cushioned. The same cannot be said for produce and fish. After brandy come fish, cut flowers, peppers and tomatoes, and for these the second column is the one that matters: more than 90% of their exports go to Russia, and in the case of tomatoes it is almost the entire crop. These groups have no alternative outlet, which means this year’s harvest has nowhere to be sold.

Growth built on re-exports

Look at the macro figures over a longer span and the pattern is clear. Total exports have quadrupled, but it is worth asking what actually did the lifting.

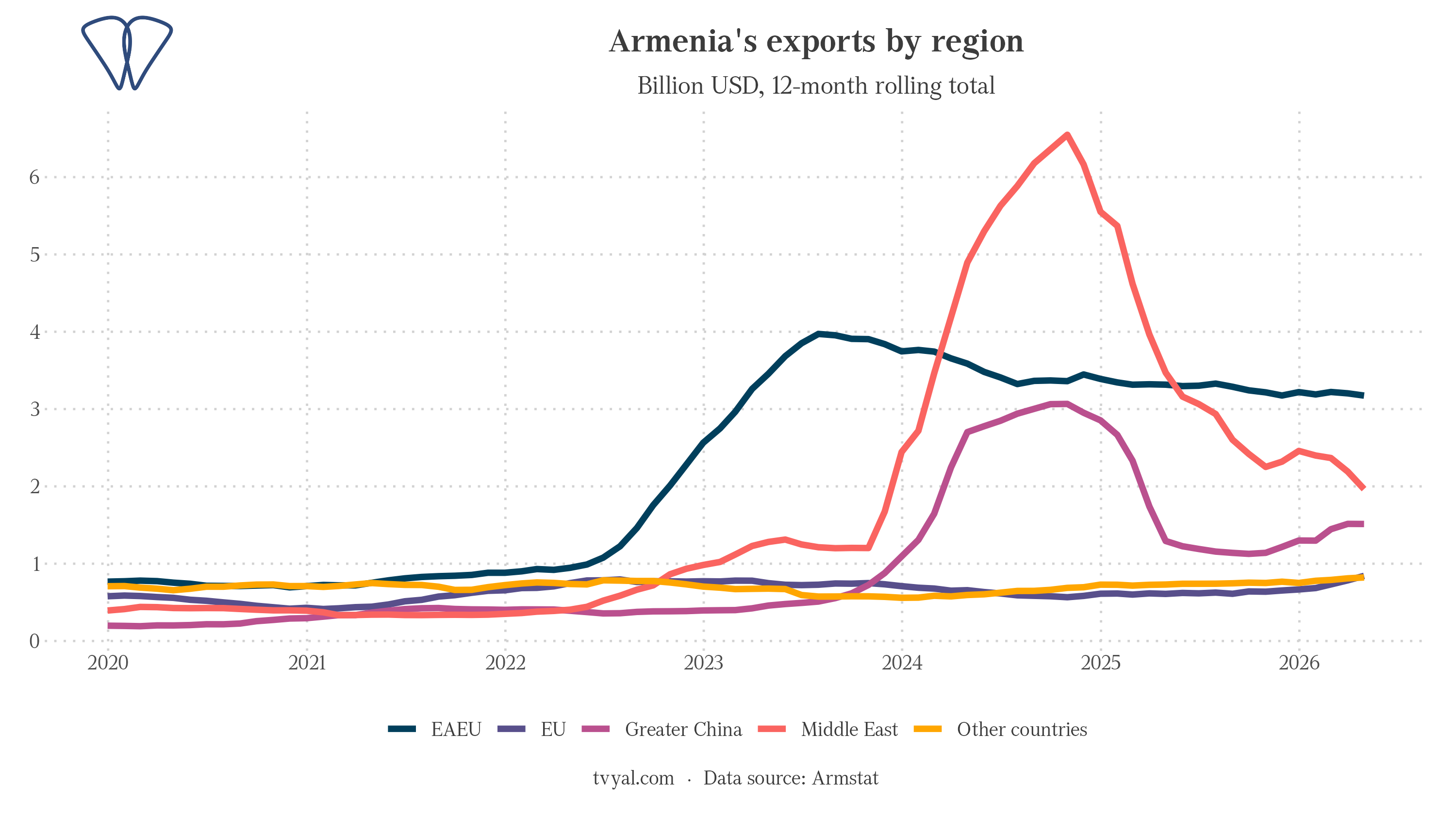

The largest importer of Armenian goods today is the Eurasian Economic Union (the dark blue line). The line that shot up in 2024 and fell back just as fast is the “Middle East” (red), and its rise came mostly from the re-export of gold and precious metals after 2022. China shows the same pattern. What looked like an export boom was really a transit corridor, one that is already running dry.

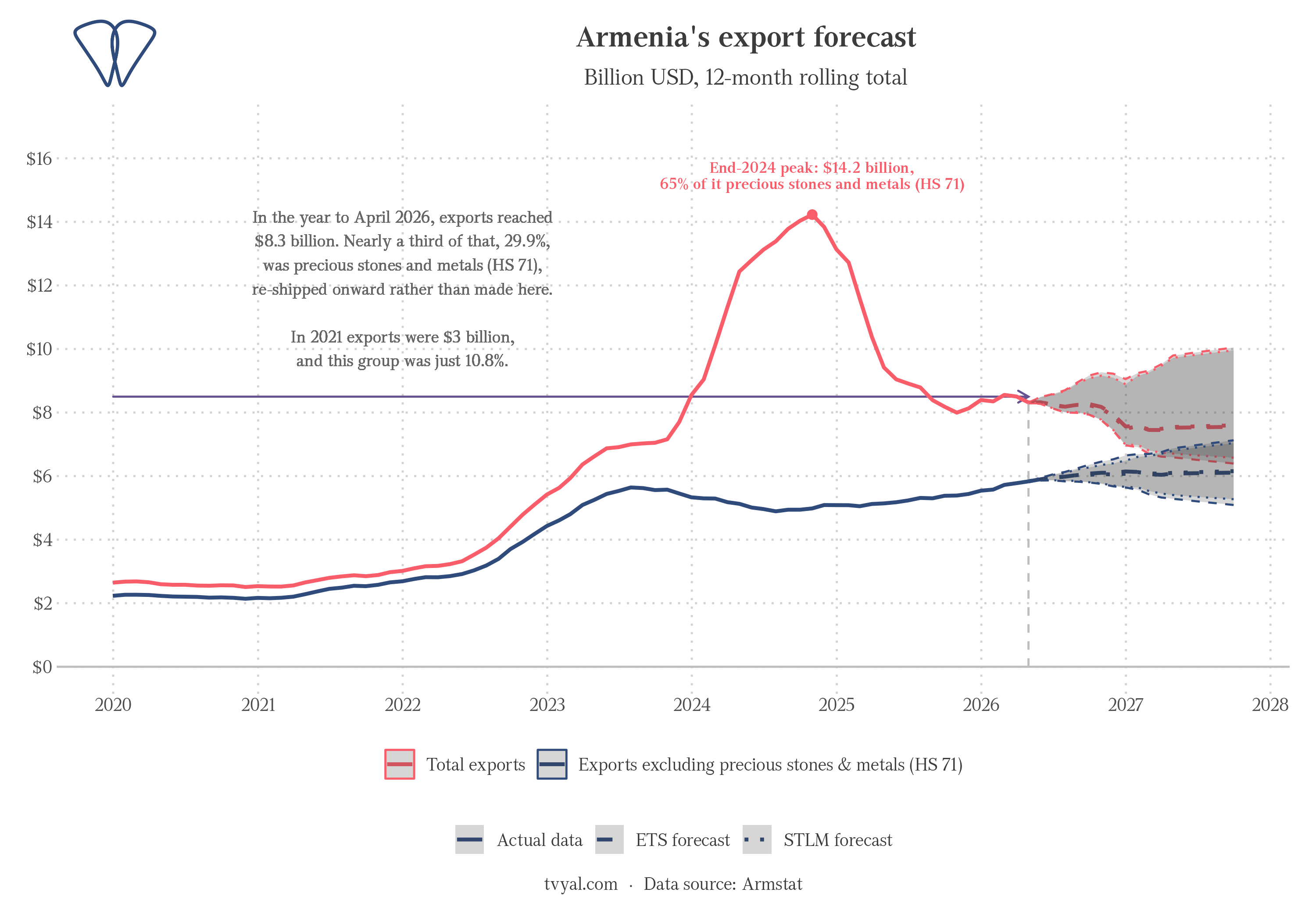

Our earlier forecast has come true, and the chart above is the proof. Its first version was published in September 2024, at the height of the gold re-export wave, when official exports were nearing the $14 billion mark. Even then our analysis showed that those figures were temporary and would settle back to their normal level. We forecast the decline while the gold was still flowing in. That forecast is now fact: the drop we projected in 2024 is a recorded statistic today.

Strip out the re-exports and the real picture is very different. Of the roughly $8.3 billion in exports recorded in the year to April 2026, nearly a third was precious stones and metals, the residue of re-export. The goods actually made in Armenia, the brandy and fish and fruit and flowers, make up a much smaller share. The bans hit precisely this vulnerable layer of domestic production. Agriculture is the one sector that kept shrinking even as overall GDP grew, and it is agriculture that now takes the blow.

Instead of diversifying and reducing risk, the dependence only deepened, and the systemic problems we now face followed from it.

What the ban costs

By the trade figures, exports of the banned goods to Russia came to about $594 million in 2025, roughly 2.4% of GDP. That matches the worst case the Central Bank’s governor set out, around 2% [2]. But the worst case assumes every dollar is lost and nothing is redirected, and in practice markets adjust to shocks.

Our neighbors’ experience is worth studying. In Moldova’s case, Russia banned wine imports in 2006 and again in 2013, citing “quality problems,” at a time when Russia was the main market. The first ban caused heavy losses, but by the second, with the EU granting duty-free access, the loss came to about a third, and Moldova reoriented toward Europe, where Romania is now its main buyer [3]. Georgia’s case matters too. Its 2006 ban on wine and mineral water lasted about seven years, and exports fell to roughly a third before the products returned to the Russian market [4]. Redirecting markets is possible, but it is slow, and it depends on a quick European response and on alternatives close at hand.

Armenia is now getting a response of that kind, at least on paper. The government plans support for exports to Europe, the United Kingdom and Canada, and the EU has pledged more than €50 million to the farm sector [5]. Taking those factors and the expected support into account, the baseline loss works out to around 1% of GDP (about $300 million), with the real hit in 2026 itself closer to 0.5%. The main risk is the brandy ban. It currently names only three producers and accounts for about half of the total exposure. If it spreads to the whole sector, the additional loss would be around $200 million.

Why one percent understates the risk

On its own, a 1% loss of GDP looks manageable. But that number covers only the list of banned goods, while the real macroeconomic risk is far wider, for three reasons.

First, much of the recent growth came on a Russian impulse. Half of the record 12.6% GDP growth in 2022 came from a surge in banking and technology, fed by capital from Russia and the relocation of IT workers. The same logic drove the 2025 growth, this time on Iranian capital, and that inflow has now dropped sharply. The 27% first-quarter growth in finance and banking in 2025 turned into a 13% contraction in 2026, a sign of deeper systemic problems. The bans coincide with the end of that financial inflow, leaving the economy without the cushion it would need to absorb the shock.

Second, perishable produce has no alternative market right now. The Moldova playbook works for wine, but not for apricots or cut flowers that have to reach the buyer within days and meet European standards our growers cannot yet satisfy. The subsidy targets, a few thousand tonnes of produce and about ten million flowers, are far too small against the volumes at risk. For this summer’s harvest there is, in plain terms, no market to sell into.

Third, the damage outlasts 2026. Market position and contracts do not come back the moment a ban is lifted. In Georgia it took years; Moldova recovered only part of what it lost. A harvest left unsold is gone for good, and the household that loses it simply loses the money and the will to farm again next year.

So treat the one-percent figure for what it is: a measure of the goods-only impact, which is already significant. It does not capture the true scale of the systemic damage. The real blow is the loss of the largest market we have, at what may be a moment of crisis, with no alternative routes and the borders closed.

For more on the structure beneath the headline growth: The Growth Wave Stalls, Exported Growth, Shrinking Fields, and the closing sanctions loophole.

* Trade data from the Statistical Committee of Armenia and the UN Comtrade database; macro estimates from the Central Bank of Armenia. Calculations and chart source code are available on GitHub.

References

[1] Russia Issues Sweeping Ban on Armenian Imports After Pashinyan’s Victory // The Moscow Times — themoscowtimes.com

[2] Russian restrictions could shave up to 2% off Armenia’s economy, Central Bank warns // CivilNet — civilnet.am

[3] Moldova’s Wine Industry Is the Latest Front in Russia’s Battle With the West // Foreign Policy — foreignpolicy.com

[4] Georgia Nationalises Iconic Mineral Water Due to Russian Sanctions // IWPR — iwpr.net

[5] Armenia launches support programme for exporters in response to Russian restrictions // JAM-news — jam-news.net