Dollar Near a 22-Year Low: Armenia's Hidden Currency Risk

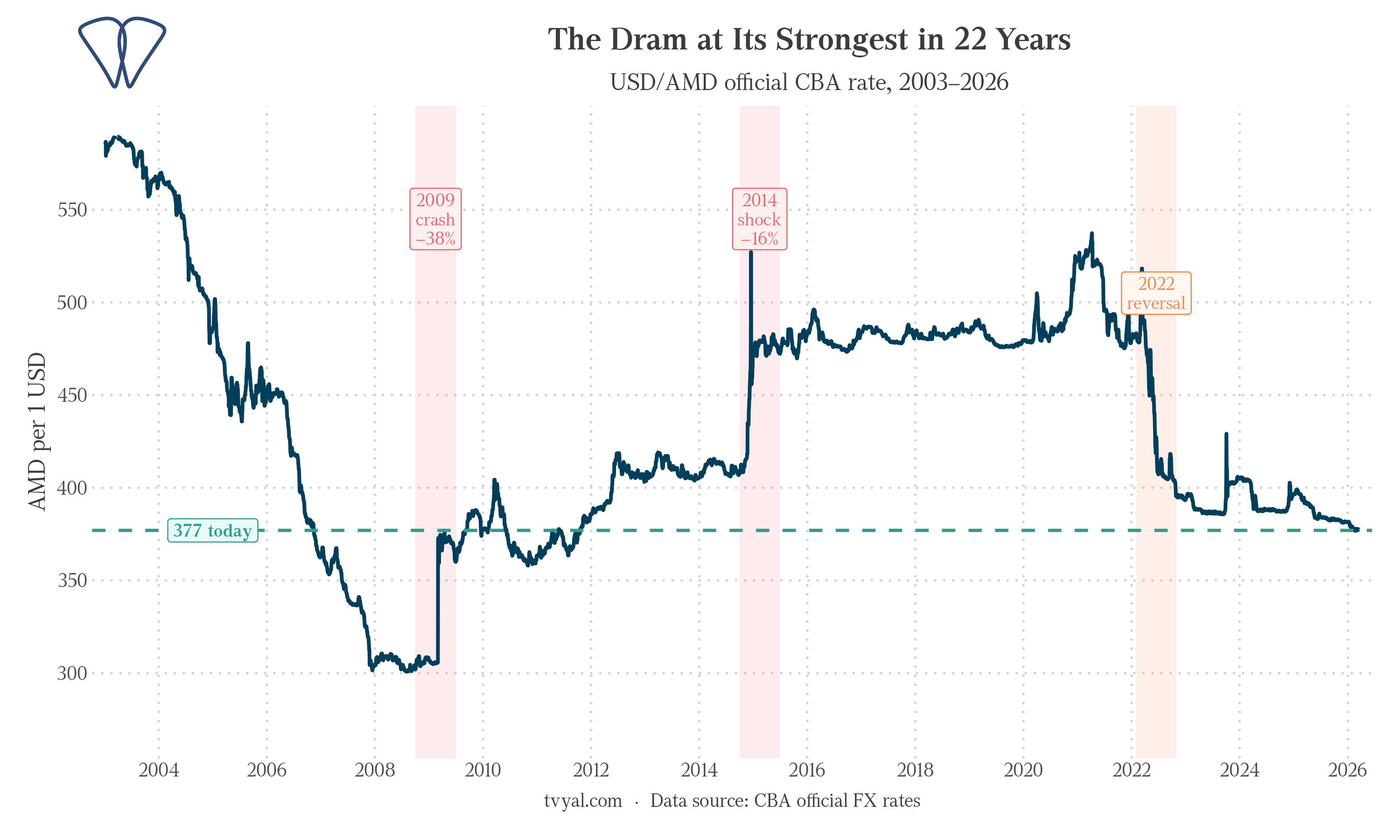

The dollar costs 377 drams today, the lowest it has been in over two decades. For importers and consumers this looks like good news. For anyone watching the Central Bank’s balance sheet, it signals that something structural is building underneath.

Three Taps Are Open at Once

Three independent sources are flooding Armenia with foreign currency simultaneously.

Russia (since 2022). Sanctions pushed Russian capital and people toward Armenia. In 2024 alone, gross inflows from Russia reached $3.82 billion (roughly 14% of GDP), turning Armenia into one of the most remittance-intensive economies in the world.[1]

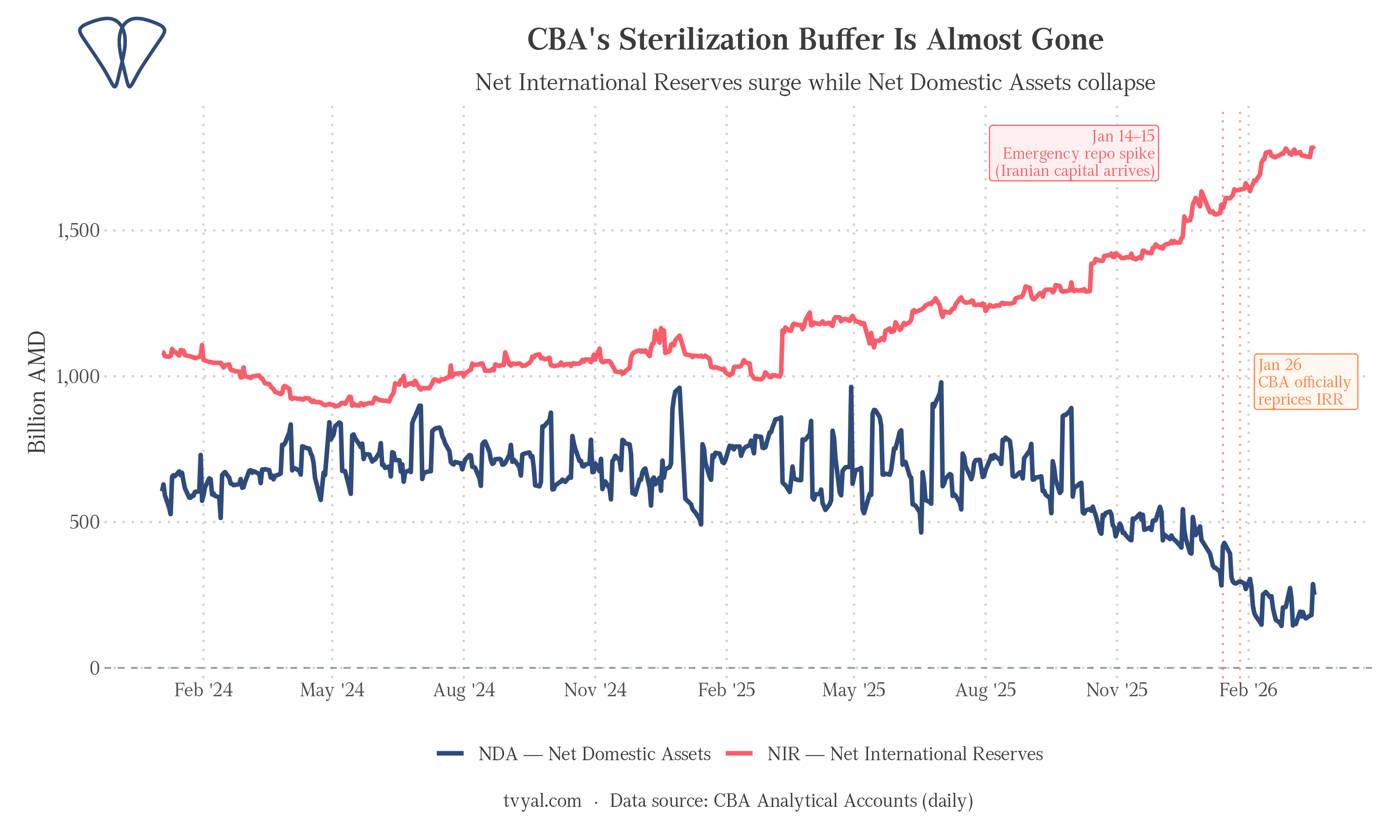

Iran (since mid-2025). The Iranian rial has been in freefall. The open-market rate crossed one million rials per dollar in March 2025, then surged to 1.47 million by January 2026, roughly doubling in under a year as the government dismantled the NIMA foreign-exchange subsidy system.[2][3] Iranians with dollar savings are routing them through Armenia’s banking system via land-border routes. The Central Bank’s own books show the timing: a 272-billion-dram emergency repo spike on January 14–15, exactly 11 days before the CBA officially acknowledged the new rial rate. The banks knew first.

Gulf capital (since early 2026). The Hormuz disruption has shaken Dubai’s role as a regional transit hub. Capital flows from Armenia to the UAE reached $880 million in 2024, the leading outflow destination, but began declining sharply in 2025 and have decelerated further in early 2026 as Gulf uncertainty grows.[4] Gulf diaspora funds are also moving inward as a precaution.

The result: Armenia’s net international reserves have risen 31% since October 2025, reaching 1.779 trillion drams.[5] The dram keeps strengthening. The market keeps betting on depreciation. The market keeps losing.

The Central Bank’s Shrinking Buffer

The CBA buys dollars to slow the dram’s rise. When it does, it injects drams into the banking system. To prevent those drams from causing inflation it issues securities and reverse repos, a process called sterilization. This is tracked in a figure called Net Domestic Assets (NDA).

NDA stood at 649 billion drams in January 2025. Today it is 198 billion, a 70% collapse in 15 months. At the current pace of capital absorption, the remaining sterilization buffer could be exhausted within two quarters. When NDA reaches zero, any new dollar arriving in the country directly expands the money supply. Armenia’s monetary policy buffer is being ground down.

Twenty-Two Years of Context

The chart above shows USD/AMD since 2003. That history has three distinct arcs. From 2003 to 2008, the dram strengthened steadily from around 560 per dollar to just 304 (the strongest level in modern history), driven by a construction boom and rising remittances. The 2009 global financial crisis ended that: the rate corrected sharply and then settled in the 400–415 range through 2013. The second break came in late 2014 when the Russian ruble crisis transmitted instantly through Armenia’s remittance channel: the dram fell to 480, briefly spiked to 580 in panic, and held near 480 for nearly six years. The paradox arrived in 2022: when the Ukraine war began, markets expected another ruble-style shock. Instead the opposite happened: capital and workers flooded in from Russia and the dram strengthened, becoming the most appreciated convertible currency in the world that year.

Today’s 377 level sits near where the dram stood in the post-2009 recovery, last seen in 2010. The 90-day annualized FX volatility is currently 1.38%. The long-run average is 3.08%. Before the 2009 crisis it was 2.6%; before the 2014 shock, 2.7%. Today’s suppression is deeper than both.

Low volatility is not stability. It is a compressed spring.

The Two-Phase Scenario

The near-term picture is continued strengthening. The dram could plausibly reach 360–370 within 12 months as long as all three taps remain open. Construction is up 21%, the highest rate since the pre-2009 bubble.

The longer-term picture is the reversal. When flows normalize (whether because Iran stabilizes, a global recession reduces Russian remittances, or Gulf capital finds new routes), all three taps may close at once. The CBA, its sterilization buffer exhausted, would defend with raw reserves. The historical playbook (2009, 2014) ends with a rapid 20–30% devaluation.

The spring is not releasing. It is being wound.

The single indicator to watch: when NDA starts rising while NIR is flat or falling, the defense has begun. That gives four to eight weeks of warning.

See also our related analyses:

* NDA and NIR series from CBA monetary survey data. AMD/USD daily series from CBA. FX volatility computed as 90-day annualized standard deviation of daily log returns.

References

[1] Net inflow of remittances from Russia to Armenia in 2024 // ArmBanks.am — https://armbanks.am/en/2025/02/04/259908/

[2] Iran rial hits new record low of 1.31 million to the dollar // Iran International — https://www.iranintl.com/en/202512153499

[3] Why Iran cannot stop its currency collapse // Iran International — https://www.iranintl.com/en/202601308271

[4] Net inflow of money transfers to Armenia from abroad increased by 8.6% in 2025 // ArmBanks.am — https://armbanks.am/en/2026/02/02/270196/

[5] Armenia’s reserves reached a record $5.2 billion in 2025 // ArmBanks.am — https://armbanks.am/en/2026/02/23/270833/